GENERAL ECONOMIC OUTLOOK

Following the referendum in Greece on 5th July which, with 61% of the votes, rejected the

reforms which the main European institution's has proposed for the Greek economy,

negotiations have once again started in Europe in order to pave the way for a third bailout

package. A week after the referendum, and following tough negotiations within the

Eurogroup and in the Eurozone Heads of State and Government Summit (in

which even the option of exiting the Euro was discussed), a unanimous agreement

between Greece and all the Eurozone countries was reached on 13th July.

The agreement is the first step towards negotiating a European Stability

Mechanism (ESM) aid programme which would allow Greece to meet its financing needs,

estimated to be between 82 and 86 billion Euros between now and 2018. In order for it to go

ahead, Athens must:

Approve structural reforms within a very limited timeframe (during the same

week as the agreement) as well as on a mid-term scale. The main reform demands are

those which affect the labour market, pensions system and banking sector. There are

also additional measures such as increasing VAT and liberalising some sectors. These

conditions are similar to those which were on the table before the referendum.

Create a public asset fund which will fall under the supervision of European

Institutions. This will be a source from which to make the additional repayments

against the new ESM loan and will generate 50 billion Euros which will be used for

bank recapitalisation, debt rate reduction and making investments.

The agreement will need to be ratified by the Greek Parliament as well as other European

parliaments. The implementation of the agreement will allow Greece to avoid

exiting the Euro, begin bailout condition negotiations for the coming years and, in

an initial phase, obtain around €12 billion to cover immediate payments and €10

billion for financial sector recapitalisation. For its part, the European Central Bank could

continue to provide the emergency liquidity assistance for the Greek financial system in order

to avoid total collapse.

The third rescue package for the Greek economy has overshadowed everything

that has happened in China's stock markets, which registered significant falls, which have

slowed in mid-July. The main stock indexes (Shanghai and Shenzhen) have fallen 30% from the

highs registered at the beginning of June with a significant knock-on effect in other Asian

markets, particularly in Japan. One possible explanation for this stock market correction is that

the bubble in the companies’ share price has burst. These stock prices had undergone an

upward rally trend which did not reflect key economic and business activity variables, which

were slowing down. The government's reaction was to take intervention measures such as a

stock purchase plan, prevent its State Reserve Fund from selling securities and, in some cases,

stop new stock listings. Whilst this episode now appears to be under control, it has opened up

a debate on the impact on the world economic outlook if there were a sharp slowdown in

activity in China.

The crisis situation in Greece and the huge falls in the Chinese stock market have

left a great volatility in the financial markets over the last month. The situation in

Greece and the uncertainty of the negotiation process, which included the possibility of a

Greek exit from the Euro, led to European risk premiums shooting up and significant falls in

stock markets. Once the agreement was reached, financial markets responded with all-round

rises in stock markets (the IBEX regained 11,000 points) and in bonds (Spain's risk premium

returned to 125 basis points). The Euro, for its part, has remained at around 1.10 dollars.

Economic Research Unit- July 2015

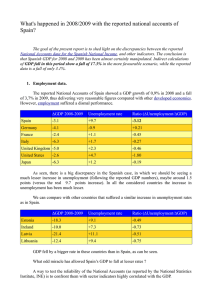

In Spain, the government has presented its new macroeconomic framework and

expenditure ceiling which will form the basis of the country's General State

Budget for 2016. Additionally, fiscal reform has been brought forward. In terms of

changes, it is worth pointing out the upwards revision of the Spanish economic forecast for

2015 to 3.3% and the stable 3% forecast for 2016. Strong domestic demand, along with the

neutral role of the net external demand, is behind this GDP increase. Employment creation will

reach 600 thousand jobs and unemployment rate will settle at 21.1% in the last quarter of

2015, going down to 19.7% towards the end of 2016. Additionally, inflation will remain stable

despite the consumption deflator upturn to 1.1% in 2016. Current account surplus will

continue at around 1.2% of GDP both in 2015 and in 2016. The IMF has also recently released

positive forecasts for the Spanish economy. For its part, it has raised growth forecast for 2015

to 3.1%, although it predicts a downturn to 2.5% in 2016.

Regarding the General State Budget guidelines for 2016, the public expenditure ceiling has

been reduced 4.4% to 123.394 billion Euros, a reduction which reflects the drop in financial

costs and unemployment. The public deficit target for all public administration bodies is being

maintained at 2.8% in 2016 with the State accumulating the largest deficit (-2.2% of GDP). The

target for regional governments has been set at -0.3% of GDP for 2016, which is the same

figure than for the Social Security. Local governments will achieve a balanced budget in that

same period.

For its part, the government has also given the go-ahead on bringing forward the income tax

fiscal reform due for 2016. That is, an estimated increase in disposable income of 1,500 million

Euros. This, along with the new social measures which have been announced (embargo

restriction, exempt social assistance) and others which affect public sector employee

compensation, could be interpreted as a sign of the end of the budget austerity policy.

In terms of more recent information on the Spanish economy, the Bank of Spain

has confirmed that the Spanish economy showed a slight upturn in growth to 1% in

the second quarter thanks to the dynamism of all domestic demand components

(particularly those related to the private sector) and an almost neutral contribution of net

external demand to GDP.

The Spanish monetary authority has also pointed out the rapid pace of job creation in the

Spanish economy which is very similar to GDP. That is, despite the fact that Social Security

registration figures for June were below those expected (only 35,000 more people

registered along with a slowing down of the year-on-year growth rate), employment figures for

the second quarter are positive. This brings the second quarter to a close with an

increase of 468,556 in comparison with the previous quarter. In year-on-year terms,

registration figures increased to a growth rate of 3.5% compared with 2.9% in the first quarter

of the year. Additionally, all sectors have made a contribution to this improvement

(construction stands out in relative terms and services in absolute terms with 361 thousand

new jobs created).

Inflation returned to positive ground in June. Taking into account June's CPI, annual

variation is at around 0.1%, above May's -0.2%. Increases in electricity and food prices are the

main factors behind this rise. As such, inflation will once again be positive, even though it will

be near zero during the central months of the year with an upturn to above 1% in December.

With this new upturn in CPI, average inflation for 2015 could stand between -0.2% and 0%.

Economic Research Unit - July 2015

0

0