THE SPANISH ECONOMY: FACTS THAT CANNOT BE

Anuncio

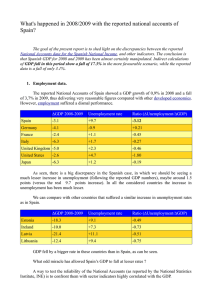

THE SPANISH ECONOMY: FACTS THAT CANNOT BE OVERLOOKED Luis de Guindos Minister of Economy and Competitiveness 6 September 2012 Accumulated Imbalances of the Spanish Economy 1. Private sector indebtedness Fast credit growth in 2003-09, encouraged by the lax monetary policy stance, was financed with external debt 2. Housing Bubble 82% increase in housing prices from 2003 to its peak in 2008 3. Loss of Competitiveness Drastic increase ( 30%) in Unit Labour Costs since joining the Eurozone Source: Bank of Spain Consequences of the accumulated imbalances 1. Deterioration of Public Finances 2. Increase in Unemployment The public deficit soared as a result of a strong discretionary fiscal expansion (reflected in the structural deficit trend) While the public deficit jumped to 11 % of GDP from a 2% surplus in 2007, the unemployment rate shot up from 8.3% to 21.6% Source: Ministry of Finance 3. Deterioration of financial sector balance sheets as a result of their high exposure to the Real Estate sector. Credit to Real Estate developers rose from €78 billion in 2003 to €324 billion in 2009, growing three times faster than total credit to the private sector. 2 On-going correction of imbalances and strengths of the Spanish economy The accumulated imbalances are in the path of being corrected The Spanish economy has significant strengths: 1. Spain is a competitive economy Trade balance in surplus with the Euro zone Good performance of exports Declining Unit Labour Costs are boosting competitiveness Fast Adjustment in the current account deficit 2. Spain is a sustainable economy The private sector is de-leveraging at a fast speed Public Finances are sustainable Spain is well prepared to address ageing population challenges Potential Growth compares well with Eurozone peers thanks to structural reforms A very sound financial sector after the new provisioning requirements and 3 restructuring regulations Spain is a competitive economy The Trade Balance is in surplus with the Eurozone since 2010 Trade surplus with France, Italy, Austria, among others The trade surplus (goods and services) with the Eurozone has recorded a fivefold increase in the fist half of 2012. The traditional trade deficit with Germany has been drastically reduced in the first half of 2012 it declined by 52% and exports to Germany grew 7.4% y-o-y. At a global level: Spain records a non-energy goods surplus and Tourist and Non-tourist services surplus. 4 Spain is a competitive economy Good performance of Exports Since 2001, Spanish goods exports have increased by 70%, the same as in Germany. Italian exports have grown by 41% and French exports by 30%. Source: Bank of Spain 5 Spain is a competitive economy Declining Unit Labour Costs are boosting competitiveness Manufacturing labour costs have decreased by more than 12% since its peak in march 2009. As a result, exports diversification is significantly improving The non-EU share in total exports has increased to 35% from 28% in 2010. Source: Bank of Spain 6 Spain is a competitive economy Fast adjustment in the current account deficit The financing needs of the Spanish economy are significantly narrowing. From a deficit of 10% of GDP in 2007, the current account is expected to be close to balance in 2013. IMF FORECAST Source: Ministry of Economy and Competitiveness for actual data and IMF for forecast The primary account balance (excluding foreign debt interest payments) is in surplus since 2011 and is improving further. 7 Spain is a sustainable economy 1. The private sector is de-leveraging at a fast speed 2. Public Finances are sustainable a) The public debt ratio is below the EU and the Eurozone average: Public Debt in 2011 in terms of GDP (Eurostat) Spain: 68.5%; EA-average: 87.2; Germany: 81.2% b) It is expected that the public sector will approach to primary surplus ( public account excluding interest payments) in 2013, ensuring the sustainability of Spanish public finances c) Strong fiscal consolidation is ongoing at all levels of Administration 3. Spain is better prepared to address ageing population challenges 4. Potential Growth compares well with Eurozone peers thanks to structural reforms 5. Financial Sector: • Aggressive clean-up of balance sheets • New legislation on a new framework for the restructuring and resolution of financial institutions. • The relative weight of the financial sector in Spain is lower than in other European economies: Ireland ( 829% of GDP); UK (603% of GDP); France (375% of GDP) Spain (326% of GDP) Germany (310% of GDP) 8 Spain is a sustainable economy The private sector is de-leveraging fast Both corporate and household debt have significantly decreased since their peak levels With the current pace of deleveraging, private sector debt will be below the EC’s reference ratio by the end of this decade 160 Source: Deutsche Bank Source: Bank of Spain 9 Spain is a sustainable economy Strong Fiscal Consolidation in all levels of Administration The Government is firmly committed to comply with the new consolidation path set up under the Excessive Deficit Procedure in July The structural adjustment effort will be huge: above 7% of GDP in 3 years (2012 until 2013) A substantial improvement in the Spanish Fiscal Framework has been adopted and is already effective • • Constitutional Reform introduced even before the Fiscal Compact adoption Law on Budgetary Stability provides for further fiscal discipline and far-reaching enforcement tools monitoring and • Ambitious Fiscal Adjustment measures have been adopted since December 2011, both on the expenditure and the revenue side. Total adjustment between 2012 and 2014 amount to more than 102 billion euros. • Fiscal recommendations addressed to Spain under the European Semester have already been implemented • The multi-annual budget plan for 2013-14 was presented by the end of July 2012, as envisaged. This plan fully specifies the structural measures to achieve the correction of the excessive deficit by 2014. 10 Spain is a sustainable economy Spain is well prepared to address the Ageing Challenge Germany Spain France US % of GDP. Age-related expenditure (per year) 2010 2020 Pensions 10,8 10,9 Health Care 8 8,6 Long-term Care 1,4 1,7 Total 20,2 21,2 2010 2020 Pensions 10,1 10,6 Health Care 6,5 6,5 Long-term Care 0,8 0,9 Total 17,4 18,0 2010 2020 Pensions 15,3 14,5 Health Care 6,6 6,6 Long-term Care 1,9 2 Total 23,8 23,1 2010 2020 Pensions 4,9 5,1 Health Care 3,1 3,4 Long-term Care 2,5 3,2 Total 10,5 11,7 Source: European Commission (2012), CBO Change 1,0 Change 0,6 Change -0,7 Change 1,2 11 Spain is a sustainable economy Growth Potential compares well with European peers Growth potential by the end of this decade Spain Italy France Germany Change in working age population 0,2 -0,2 0,0 -0,6 Change in employment ratio Change in productivity POTENTIAL GDP GROWTH 0 1,2 1,4 0,4 0,1 0,3 0,1 1,2 1,3 1 1,2 1,6 Source: Deutsche Bank According to Deutsche Bank calculations, the potential GDP growth of Spain is similar to Germany’s and France’s and bigger than Italy’s, thanks to the structural reforms implemented 12 Spain is a sustainable economy Aggressive Clean-up of Balance Sheets Coverage of Real Estate assets linked to loans to developers (€ 307 billion). Coverage of Real estate assets linked to loans to developers Coverage of Real estate assets linked to loans to developers (in percent) (in € bn) Problematic Assets •Total provisions + capital buffer → € 100 bn •Total Balance → € 184 bn Performing Assets •Total provisions → € 37 bn •Total Balance → € 123 bn TOTAL •Total coverage → € 137 bn •Total Balance → € 307 bn 13 Spain is a sustainable economy Results of the Financial Sector Clean-up After the cleaning-up, Spanish Banks will be among the strongest in Europe Goldman Sachs research on European Banks – Supervisory metrics and Ranking Quartile on Rank 1 2 3 4 5 6 7 8 9 10 Bank Leverage Santander (post RDL) 2nd Banco Popular (post RDL) 1st BBVA (post RDL) 1st Erste Bank 3rd Bankinter (post RDL) 3rd Sabadell (post RDL) 2nd Intesa SanPaolo 1st Commerzbank 3st Banco BPI 2nd Société Générale 4th NPA coverage Liquidity (chg.) 1st 1st 3rd 1st 3rd 1st 1º 1st 2º 1st 3º 1st 2º 3rd 1º 2nd 2º 3rd 1º 2nd Sum 4 5 5 5 6 6 6 6 7 7 Source: Goldman Sachs 14 Far-reaching Structural Reforms have been implemented to boost the flexibility and competitiveness of the Spanish economy Main structural reforms already implemented 1. 2. 3. 4. 5. Labour Market Reform Financial Sector Reform Retail sector: liberalization of opening hours and elimination of restrictions on sale activities Liberalization of the Housing rental Market Health and Education A Labour market reform to foster wage moderation and job creation Main measures adopted: Firm-level wage bargaining prevails over national, regional or sector agreements Collective dismissals without administrative authorization are allowed for firms posting falling profits for three or more consecutive quarters Elimination of procedural wages Convergence of dismissals costs to the EU average • Unfair dismissal: severance pay 45 days up to 42 months 33 days per year worked up to 24 months • Fair dismissal: severance pay of 20 days per year, up to 12 months Clarification of objective causes for fair dismissal Creation of a new permanent contract directed at SMEs 15 Further strengthening of the Financial Sector: A new framework for Bank Restructuring and Resolution Legislation was adopted on August, 31st setting up a new framework for the restructuring and resolution of financial institutions Essential tool in the crisis management of financial institutions Sets up a comprehensive framework to deal with financial institutions in stressed situations. Reinforcement of intervention tools at all stages of crisis management: 1. Early intervention for mild difficulties 2. Restructuring measures for institutions with temporary troubles that can be solved with public support 3. Orderly resolution for non-viable institutions Early introduction of provisions foreseen in the future European Directive on Bank Recovery and Resolution currently under negotiation at the EU level Establishment of an Asset Management Company (AMC) 16 An ambitious economic Reform Agenda for the Second Semester 2012 The reform agenda will gain momentum this Autumn – Measures: 1. A Market Unity Law will be adopted to ensure that all goods and services lawfully produced in one Region can be supplied in all others without any additional formalities 2. National Competition and Markets Authority Law to improve the efficiency and quality of supervision 3. Further Liberalization of Professional Services to foster competition and market access 4. Energy Market reform to increase efficiency and solve the electricity system tariff deficit 5. Developing new funding sources for SMEs to reduce dependence on commercial banking funding 6. Putting the Autonomous Regions Liquidity Fund in function to help Regions to face their liquidity constrains Resources amounting to 18 billion €. 7. Completing remaining steps envisaged in the MOU: Regulatory development of the Asset Management Company (AMC) Presentation of recapitalisation plans identifying how capital shortfalls will be covered Presentation and adoption of restructuring plans and injection of financial assistance into banks by November 17