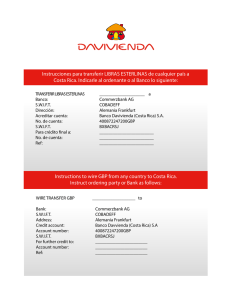

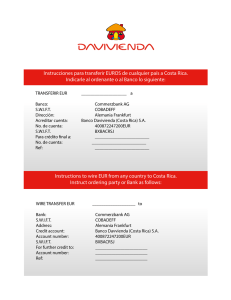

INSTITUTO COSTARRICENSE DE ELECTRICIDAD

Anuncio