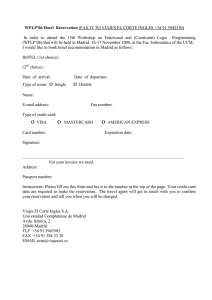

Main Figu of the AC

Anuncio