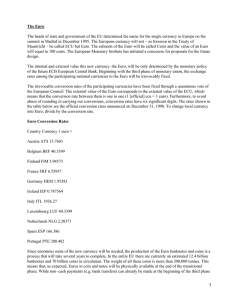

Implications for the euro area of divergent monetary policy stances

Anuncio