Centre of Expertise for Local Government Reform

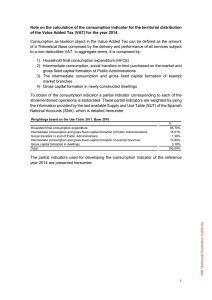

Anuncio