At a Glance

ECONOMIC AND MONETARY AFFAIRS

IFRS Accounting Standards Endorsement Procedure

International Financial Reporting Standards (IFRS) i

are issued by an international private organisation,

the International Accounting Standards Board (IASB).

In order to become binding law in the EU, they must be ‘endorsed’ in a specific procedure

prescribed in Article 3(1) and 6 Regulation No 1606/2002 of the Parliament and of the

Council (consolidated version) and Articles 5a(1)-(4) and Articles 10 and 11 Council

Decision 1999/468/EC (consolidated version), i.e. the ‘Regulatory Procedure with

Scrutiny’ ii (FR ‘PRAC’). All standards and interpretations are adopted as Commission

Regulations (Regulations to amend an annex to Commission Regulation No 1126/2008,

consolidated) to have directly binding effect without the need for national implementation.

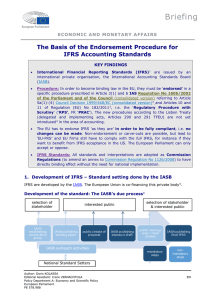

Development of the standard: The IASB’s due process iii

selection of

stakeholder

IASB

establishing

consultative

group

selection of stakeholder

& interested public

interested public

IASB publishing

working paper

public debate of

proposal

IASB publishing

exposure draft

IASB outreach activities

public hearings

and/or field

studies

IASB publishing

final IFRS

nonmandatory

steps

mandatory

steps

National Standard Setters

EU Endorsement of IASB issued standards iv - best case scenario

EFRAG & COM effect study

Impact Assessment

EFRAG advice

Commission

proposal

stakeholder consultation

Author: Doris KOLASSA

Editorial Assistant: Irene VERNACOTOLA

Policy Department A: Economy and Scientific Policy

European Parliament

PE 569.995

EFRAG European Financial Reporting Advisory Group

ARC

Accounting Regulatory Committee

ARC vote

Council and

Parliament

scrutiny

endorsement

decision

possible opposition by ARC, Council/EP,

see next page

EN

Policy Department A: Economic and Scientific Policy

Possibilities for EU Endorsement of IASB issued standards

requests EFRAG opinion on IFRS standard

endorsement advice within 2

months: positive if consensus,

QM or simple majority, stating

dissenting views

European Commission

Accounting

Regulatory

Committee

(ARC)°

negative or no

ARC opinion

positive ARC

opinion (QM)

Commission submits proposal to Council

and forwards it to EP

Commission submits proposal for scrutiny

to Council and EP

no Council/EP

opposition

within 3

months from

referral date

Regulation

is adopted by COM

Council (QM)

or EP (AM)

oppose^

within 3

months

Council (QM)

opposes^

within 2

months

i) Council

envisages adoption

and submits to EP

ii) Council does not

act within 2

months: COM

submits to EP

EP does not

oppose or

react within

4* (resp. 2)

months

Regulation

cannot be

adopted by

COM

but: Commission may submit ‘amendedi’ (e.g.

carve-out) or ‘new’ (or old unchanged) proposal to ARC

Legend:

QM = qualified majority; AM = absolute majority (of component members)

Regulation

is adopted by COM

°ARC delivers opinion with time limit set by its chair, voting with QM, but may refrain from an opinion

^opposition must be justified and can be based only on (i) an excess of implementing powers, (ii) noncompatibility with basic act, or (iii) disrespect for subsidiarity/proportionality

*period calculated from the initial forwarding date (as Council has two months)

i

ii

iii

iv

IFRS are issued by the IASB. The EU has to endorse IFRS 'as they are' in order to be fully compliant,

i.e. no changes can be made. Non-endorsement or carve-outs are of course possible, but then they

become ‘EU-FRS’, and EU firms have still to comply with the full IFRS if they want to benefit from

IFRS acceptance, e.g. in the US.

The Commission has currently no proposal to align the pre-Lisbon-Treaty PRAC to the new

delegated/implementing acts procedure according to Articles 290 and 291 TFEU.

Source: Botzem, The EU’s Role in International Fora: Paper 7-The IASB, 2015, p. 24.

Source: Botzem, p. 27, based on http://www.iasplus.com/en/resources/ifrs-topics/europe.

DISCLAIMER

The content of this document is the sole responsibility of the author and any opinions expressed therein do not necessarily

represent the official position of the European Parliament. It is addressed to Members and staff of the EP for their parliamentary

work. Reproduction and translation for non-commercial purposes are authorised, provided the source is acknowledged and the

European Parliament is given prior notice and sent a copy.

This document is available at: www.europarl.europa.eu/studies

Contact: [email protected]

Manuscript completed in May 2016

© European Union

Internal ref.: ECON-2015-14

ISBN: 978-92-823-8677-4 (paper)

ISBN: 978-92-823-8678-1 (pdf)

CATALOGUE: QA-01-16-089-EN-C

CATALOGUE: QA-01-16-089-EN-N

doi: 10.2861/836729 (paper)

doi: 10.2861/58642 (pdf)

0

0